How to benefit from different valuation perspectives.

The process of calculating and assigning a value to a company is called valuation. Not everyone investing in the stock market is concerned about the value of a company.

- If you are a trader buying and selling pieces of paper based on technical indicators, you are probably not concerned about the value of the company.

- If you are a smart beta investor or even an indexer, individual company performance may be less important than macro indicators eg interest rate, and economic performance.

But if you are a value investor whose buying and selling signals are based on comparing the market price with intrinsic value, then the valuation is key.

There are several ways to value a company and invariably you will get different answers using the different approaches. The practice is to then try to triangulate a value.

I would argue that instead of trying to triangulate a value, there are benefits to having different values.

Contents

- Methods of valuation

- Strategic insights

- Risk and valuation

- What could go wrong

- What to use

- Conclusion

Methods of valuation

There are 3 general ways to value companies

- Relative valuation

- Asset-based valuation

- Earning-based valuation

The simple way to understand them is to use the analogy of how properties are valued.

1) Relative valuation is valuing your house based on the comparable value of houses in your neighbourhood. You might scale it to account for some of the differences in the properties.

Following this logic, if comparable companies are trading at 10 times their earnings, your company should also be worth 10 times their earnings. Other common bases of comparison are book value, net tangible assets, and revenue.

2) Asset-based valuation (AV) is valuing your house based on what it cost to buy the land and build the house. You might use the historical cost to serve as the floor value or you might use the current cost.

There are several ways to determine the value of companies when using this approach. For example, we could use the book values, the revised net asset values, and even the reproduction values.

3) Earning-based value (EV) for your house is the present value of all the net rental income over its life. You will of course have to decide on the appropriate discount rate to use to compute the total present value.

In the context of valuing companies, we have the discounted cash flow method. The variables to consider are then what to use as the cash flow, which discount rate to use, and how to account for the life of the business.

Since valuations are based on assumptions, the likelihood is that the values for a particular company obtained from using the above 3 methods will not be the same. That is why people talk of triangulating a value so that there is a common number.

But I would argue that there are insights and benefits to having different answers.

Strategic insights

It was Professor Bruce Greenwald, Columbia Business School who inspired me on what to do with the different values. He opined that an analysis of the AV relative to the EV provides some insights into how well the company has deployed its resources.

There are 3 possible scenarios when comparing the EV with the AV as illustrated below.

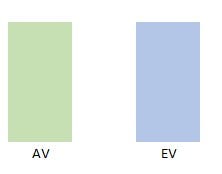

Scenario 1: EV = AV. This is the most common situation where the return is equivalent to the cost of capital. In a competitive environment, a business with high returns would attract competition. Eventually, any excess returns would have competed away so that the company just earn its cost of capital.

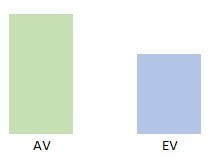

Scenario 2: EV < AV. In this case, the assets are under-utilized possible due to some issues with the business. This could be due to poor management, or that the business in an industry is in secular decline. You could also get this scenario if the company has a lot of non-operating assets eg cash in its books.

Scenario 3: EV > AV. In this case, the returns generated by the business far exceed the cost of capital. I would expect the company to have some form of an economic moat for it to continue to enjoy a return that is higher than the cost of capital.

In practice, it is unlikely to have a situation where the AV exactly matches the EV. So, I have assumed that AV = EV is when the computed difference is within +10% or -10% of each other.

What can you do with such a comparison?

- If I am analyzing a mature company, I would expect to find Scenario 1.

- If I am analyzing a company undergoing a turnaround, I would expect to see Scenario 2.

- If I am analyzing a company that can continue to compound shareholders’ value, I would be shocked if I don’t see Scenario 3.

If there is a disconnect between the Scenarios and the business situation of the company, I would first check my assumptions and analysis. It is a good sanity check. I would be most happy when I cannot find anything wrong with my assumptions and analysis as it indicates an investment opportunity.

Risk and Valuation

My next step would be to compare the AV and EV together with the market price to get a sense of the margin of safety.

Warren Buffet considered “margin of safety” as the 3 most important words in investing. The concept of the margin of safety in investing was popularized by Benjamin Graham, the father of value investing.

It refers to the extent to which the market price of a company is below the estimates of its intrinsic value. It offers you some protection in case you made some error in estimating the intrinsic value.

You make many assumptions in valuing companies. Just because it is mathematically correct does not mean that it reflects reality. The margin of safety is recognizing this imperfection.

At the same time, the margin of safety is also an indication of the potential upside for the investment.

I look at the margin of safety in the context of the AV and EV analysis with the following 4 scenarios:

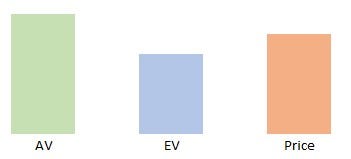

Scenario 1: Excellent margin of safety. In this case, the market price is significantly below both the AV and EV.

Scenario 2: Acceptable margin of safety. In this case, the market price is higher than the EV but lower than the AV. If you invest in a company under this scenario, it must be because you believe that the company would be able to turn around and that in the worst-case scenario, the value of the assets would offer some protection if the business fails.

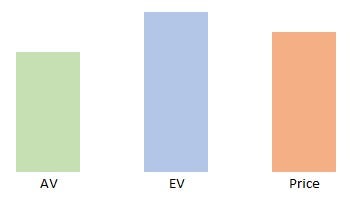

Scenario 3: Better than an acceptable margin of safety. In this case, the market price is higher than the AV but lower than the EV. In this scenario, you believe that the company’s competitive edge would provide you with some margin of safety.

Scenario 4: Poor margin of safety: In this case, the market price exceeds both the AV and EV. The only rationale for investing in such a company is that you believe that the EV will increase over time i.e you believe that this is some growth company whose future value has yet to be captured in the current EV.

What could go wrong?

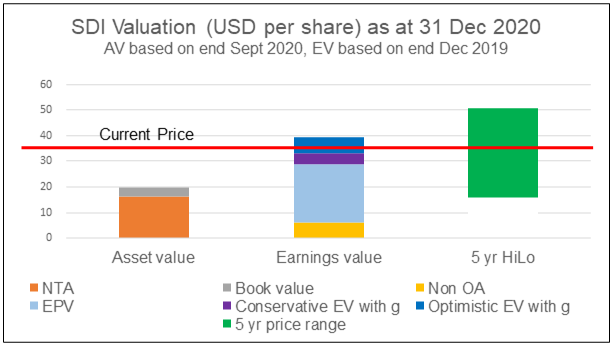

I recently analyzed a steel company and found that the EV far exceeded the AV as illustrated by the chart below. Refer to “Is Steel Dynamics a reverse value trap?”

I have checked and I stand by my assumptions. But steel is not exactly a growth sector. While my analysis showed that Steel Dynamics is a fundamentally strong company with good growth prospects, I was puzzled by this discrepancy between the AV vs EV and the nature of the business.

It turned out that Steel Dynamics had an aggressive share buyback programme. As of the end of Dec 2020, the company had shareholders’ funds of USD 4.3 billion. But over the past 5 years, the company had spent USD 1.3 billion to buy back its shares. Without these share buybacks, the AV would be higher by 30%.

OK, there is still a discrepancy between the revised AV and EV. I am sure that if I traced all the share buybacks from when the company first got listed, it would narrow the discrepancy.

I am also sure that by reducing the number of outstanding shares with the share buyback programme, the EV per share is boosted.

- At the end of 2015, the company had 242 million shares outstanding.

- This was reduced to 212.3 million by the end of 2020.

If there was no share buyback, the EV per share would be reduced by about 13 %. Of course, you would also have to adjust the asset value by the additional shares if there was no buyback.

When you factor in the impact on the AV and the EV, the differences between them narrow significantly. If nothing else, this example shows that you should not take the difference at face value.

What to use

In practice, there are different interpretations of even the AV and the EV.

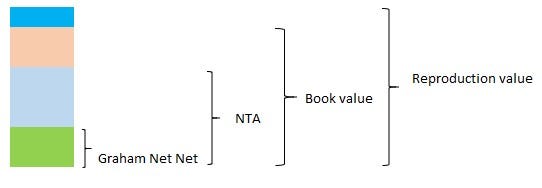

In the context of the AV, you can build up a picture of the total asset value based on the four components as illustrated below.

Information to determine the Graham Net-Net, NTA, and Book value is generally extracted from the Balance Sheet. If the company has adopted the fair value accounting rules in preparing its accounts, the values are reflective of the market price. However

- There are instances where the value of properties has been captured at historical costs. In such instances, if the value of the properties is significant, I do adjust it to reflect the current market price.

- Do not be surprised if occasionally you come across negative Graham Net-Net. In such cases, I treat this as zero.

- The most challenging to determine is the Reproduction Value. You are trying to estimate what it takes to re-create the company with all its customers’ relationships, product branding, and any R&D that has been charged out. For some sectors, you may have to reduce the value of its Plant, Property, and Equipment as it is now possible to build a new plant cheaper due to technological progress.

- For property-based companies with significant landbank, many analysts estimate what is known as the RNAV — the Revised or Re-valued Net Asset Value. The most reliable way to estimate the RNAV is to base the property value on a professional valuer’s assessment.

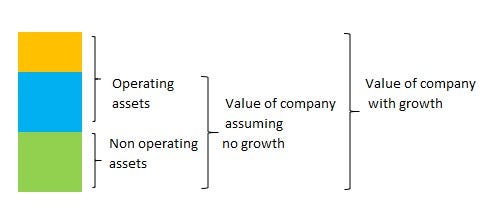

You can also build up a picture of the total earnings value as illustrated below.

What are some of the challenges I have found in using the Earnings-based valuation method?

- Growth does not add value unless the company’s return is greater than its cost of capital. If you work out the numbers for such a case, you will find that the value with growth would be less than the value without growth. In such cases, I ignore the value with growth.

- Some companies retain a significant amount of cash. I have occasionally come across cases where the market price is around the value of cash and other non-operating assets.

Then there are two ways to perform a DCF. You can use the Free Cash Flow method or the Residual Income approach. For details refer to “The Basics Of Valuation — Picking out Value Traps”.

If there are significant differences between the value from the Residual Income method compared to that from the Free Cash Flow method, I choose the Residual Income method. You will meet such situations if the company has an expansion programme. It will then require significant capital expenditure that will affect the value using the Free Cash Flow method.

If you are valuing a conglomerate operating in several different sectors, the risks and hence the cost of capital will be different for the various sectors. In such cases, you have to do more work to first value the various sectors independently. Then add them all up to get the value of the conglomerate — the sum of the parts valuation.

If you accept that valuation is based on assumptions, the best approach is then to consider all the components. The Steel Dynamics valuation as illustrated in Chart 9 is my preferred presentation.

I focus on the NTA when looking at AV and the Earning Power Value (ie earning value assuming no growth) when looking at EV. They have the least assumptions associated with each of the respective approaches.

My main point is that knowing how the numbers build up is probably more important than trying to get a single number.

Conclusion

All valuations are based on assumptions. You should not be surprised to find different values for the same company using different valuation approaches.

The advice is generally to triangulate the values so that you have one value that can be used in your assessment.

But I would argue that there are benefits and advantages of having different values.

- They can provide strategic insights into the business.

- They provide a better sense of the margin of safety.

Furthermore, if you break down the Asset Value and Earning Value into their respective components, you can have a better sense of the value of the company.

Value investing insights

If you found this article useful, you can get more insights from my book “Do you really want to master value investing?”.

The e-book is now available from Amazon, Kobo and Google Play.

PS: If you are in Malaysia or Singapore, the e-book can only be download from Kobo and Google Play.